Repaying Student Loans

You can plan your repayment strategy to work for you.

If you owe money to the federal government for the Direct loans that helped cover the cost of your education, you’re not alone. A majority of college graduates are in the same boat. Fortunately, there are a number of ways to structure repayment to make it affordable—something that’s not always the case with private loans.

What you have to recognize, though, is that it’s your responsibility to make the system work. That means two things:

Always pay what you owe each month on time.

Be sure you’re in the right repayment plan for you.

REPAYMENT BEGINS

When you graduate, are enrolled less than half-time, or drop out, you have a six-month grace period in most cases before your first loan payment is due. During that period you’ll hear from your loan servicer—the company that bills you and collects your payments—that you’re enrolled in the Standard Repayment Plan.

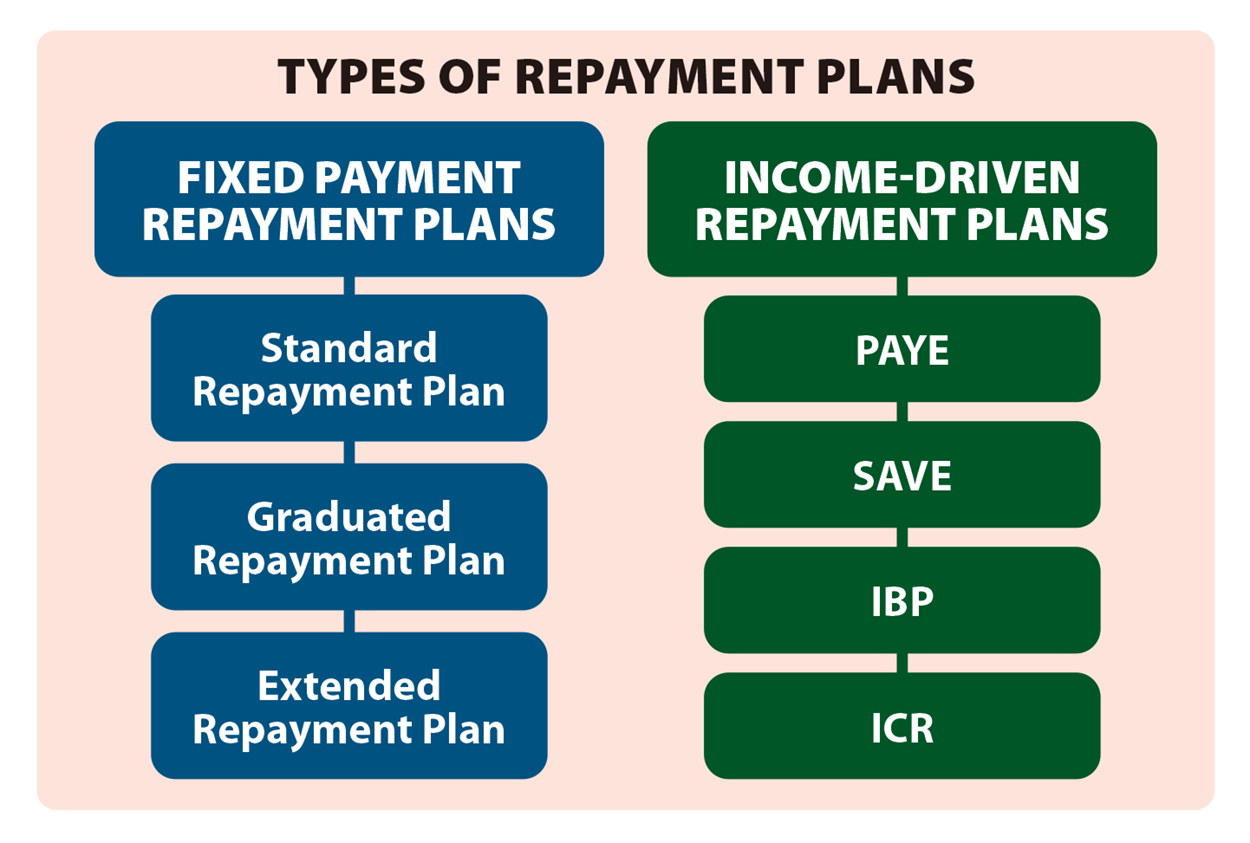

That may be fine for you. The payments are fixed, and you’ll pay off your loan within ten years. But it’s also possible the payments will be more than you can comfortably afford. So early in the grace period you should use the loan Repayment Estimator (https://studentaid.gov/aid-estimator/) to find out which other plans you qualify for, an estimate of the monthly cost, and the conditions that apply. Currently, the alternatives include the Graduated Plan and the Extended Plan. With the Graduated Plan, your payments start low and increase every two years. With the Extended Plan, your monthly payments may be fixed or gradually increase, and you have up to 25 years to repay.

If you think one of your alternatives would make it easier to keep up with your payments, you should tell the servicer you want to change plans.

It’s your right to switch if you qualify, either initially or at some time in the future if your economic situation changes. The process often, but not always, is handled efficiently. But if it isn’t, you’ll have to advocate for yourself. If you need help, you can contact the National Consumer Law Center’s Student Loan Borrower Assistance Project or the Consumer Financial Protection Bureau.

REPAYMENT ALTERNATIVES

Among the alternatives to the Standard plan are four income-driven plans that link your monthly payment to your discretionary income, or what’s left of your gross income after taxes and necessities including housing, food, and clothing. The plans, including the Pay As You Earn (PAYE) Plan, Saving on a Valuable Education (SAVE) Plan, the Income-Based Plan (IBP), and the Income-Contingent Plan (ICR), do differ in ways that may make one better for you than the others. But each of them is a good choice if you hope to qualify for Public Service Loan Forgiveness (PSLF).

Outstanding balances on these loans will be forgiven if you’ve made payments for 20 years, or 25 in some cases, though you may owe income tax on the amount that’s forgiven.

Two other possibilities are the Graduated Repayment Plan, which has a 10-year term and payments that are lower in the initial years and higher later, and the Extended Repayment Plan, which has a 25-year term with either fixed or graduated payments.

Finally, if you have older loans, including FFEL Plus Loans or FFEL Consolidated Loans, you might consider the Income Sensitive Repayment Plan.

POSTPONING PAYMENTS

If it becomes hard for you to repay your federal student loans and you are unable to change your plan to reduce the monthly payment, you may find temporary relief by qualifying to suspend your payments for a limited time.

If you’re in school at least half time, if you’ve taken parental leave, you’re unemployed, unable to work, or if you’re in the armed forces or the Peace Corps, you can apply for deferment. If it is granted and your loans are subsidized, interest isn’t due on your loan principal while you’re not paying. Unsubsidized loans will accrue interest, however, which may be added to the balance you already owe.

If you don’t qualify for deferment, you may request a forbearance. If it’s granted, your payments will be suspended for a limited time, but interest will accrue on your loan and be added to your principal balance.

But suspending payments isn’t a long-term solution to avoiding default and its negative consequences. So you’ll want to work with your servicer to resolve your debt.

LOAN CONSOLIDATION

If, as students typically do, you took several federal loans, potentially with different interest rates and different servicers, keeping track of what you owe and to whom can be a challenge. One solution may be to consider taking a federal Direct Consolidation Loan. There’s no charge, and you’ll end up with a single monthly payment.

Consolidated loans have a fixed interest rate calculated as an average of the rates on the loans you’re consolidating. The repayment term can be up to 30 years.

There are some potential drawbacks, such as the potential for paying more interest and the possibility of losing certain benefits, such as eligibility for loan forgiveness or the discount for regular electronic debit of your account. You’ll want to weigh the limitations against the convenience of a single payment.

One warning: You may be offered loan consolidation deals from private lenders. You almost always make out better with the government option.

OTHER LOANS

If you’ve taken loans from private lenders, the terms of repayment may be less flexible that those of the Direct Loan program. But they must also be repaid.

SERVING THE PUBLIC

If you work in a qualifying public service job for 10 years, you may be eligible for loan forgiveness after making 120 payments in an income-driven plan. Be prepared, though. The eligibility rules are changing in July 2026, so be sure to get the updates at www.studentaid.gov.

VIRGINIA B. MORRIS is the Editorial Director of Lightbulb Press. A noted expert on financial literacy, Virginia serves as a sought-after consultant on investor education. She has written more than forty books on financial subjects, as well as articles, white papers, financial literacy websites. She is responsible for Lightbulb’s accessible approach to explaining investing and personal finance.

Virginia holds a PhD and an MA from Columbia University.